Or more useless theory that doesn’t get you any closer to your goals.

Not everyone is right for Getting Started With Python for Quant Finance and I want to make sure I don’t waste your time.

You’ll love this course if:

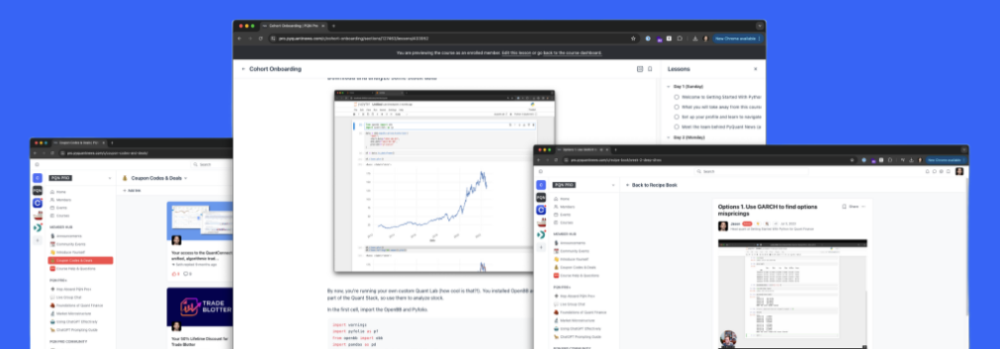

You want to use Python for getting market data, analyzing the financial markets, backtesting, and automating trading

You’re sick of paying Udemy and Datacamp for courses that are irrelevant to your goals

You want a somewhat opinionated approach to installing Python, writing code, and using the Python Quant Stack

You’re brand new to Python, quant finance, or both

You realize that taking tutorial after tutorial does not guarantee success. You want to learn and adopt of framework that will make you successful using Python

You don’t have time to waste learning a programming language and want to know just want you need

You want step-by-step guidance and structure from someone who’s been in the industry for 23 years

You like specific, hands-on instruction and don’t have time for the fluff

You’ll want a refund if:

You’d prefer to learn the theory behind programming and quant finance and not actually apply anything in practice

You prefer “figuring it out yourself” with a plethora of lessons with no clear path

You’re hoping that buying a course like this will give you trading strategies that will print you money

You’re looking for another Python tutorial that will help you do things like print “Hello World” and the Fibonacci sequence to the screen

You don’t really need to use Python in your field and probably won’t anytime soon

You’re OK with using the tools you have (like Excel) and are unwilling to budge in the slightest.

You’re thinking this course will teach you fundamentals of computer science like memory management.

You want to use Python to brute force optimize backtests and data mine the market (a bit of an inside joke you’ll understand once you dig into the course!)

There are no reviews yet.

You must be <a href="https://wislibrary.net/my-account/">logged in</a> to post a review.