🎁 HAPPY NEW YEAR 2026! Exclusive 30% OFF for New Year 2026! Use code NEWYEAR30 ✨

Claim Your Gift

Quantifiable Edges Bundle

Rob Hanna of Quantifiable Edges was named the 2024 recipient of the National Association of Active Investment Managers (NAAIM) Founders Award for his research paper “Chicken & Egg: Should you use the VIX to time the SPX? Or use the SPX to time the VIX?”!

You may download the paper at the NAAIM website or from SSRN.

Quantifiable Edges Courses

Quantifiable Edges offer 3 different trading courses. All view market edges from a quantitative perspective. All also have tools that would help traders further explore ideas on their own (spreadsheets, code, etc).

The Quantifiable Edges VIX Trading Course

The Quantifiable Edges Market Timing Course

The Quantifiable Edges Swing Trading Course

Quantifiable Edges Subscriptions

Quantifiable Edges has been publishing quantitative research, systems, and trading ideas since 2008. We utilize technical analysis concepts and quantify them in a way that allows traders to determine the edge that was provided in the past. Gold and Silver level subscribers are led through Rob Hanna’s interpretation of the data in a simple and complete manner via the nightly and weekly subscriber letters. Gold subscribers also have access to our subscriber area, which includes the Quantifinder, Seasonality Calendars, trading systems (with code), special research, and more.

Subscribers also have access to the full archive of letters back to 2008, which include thousands of original studies.

Beginner, advanced, and institutional traders have all taken advantage of the research, teachings, and tools provided by Quantifiable Edges since 2008. Free trials to the gold subscription service are offered with just name and email required. You may follow Quantifiable Edges on YouTube ( @quantifiableedges9338 ), X (Twitter)(@QuantifiablEdgs), or receive blog posts and updates from Quantifiable Edges directly to your email.

Quantifiable Edges Recent PostsView All

July Remains King of Day 1 Performance

Posted onJune 28, 2024byRob Hanna

Since the late 80s there has been a tendency for the market to rally on the first day of the month. One theory on why this occurs is that there are often 401k inflows that are put to work on the 1st of the month. I examined this tendency and broke it down by month here on the blog a few times over the years. I decided to update the study again today.

As you can see, July has both the highest Win % and the largest Avg Trade. So maybe some of that July magic will help the bulls on Monday. I’ll also note that August has had the worst Day-1 performance of any month. Below is a more detailed look at how July has played out.

Impressive stats and curve. And the last 13 instances have all been winners. Traders may want to keep this in mind.

Talking VIX Trading and my NAAIM whitepaper with Andrew Swanscott

Posted onMay 31, 2024byRob Hanna

I had the pleasure of joining Andrew Swanscott on the Better System Trader podcast on Wednesday afternoon. We had a detailed discussion about VIX trading and my recent whitepaper that won the NAAIM Founders Award. It had been a long time since I was last on Andrew’s podcast, but he is always a fun person to speak with! I hope you enjoy it.

You can also find it on your favorite podcast channels. If you haven’t listened to Better System Trader before, be sure to check it out. Andrew is a great interviewer and has a long list of interesting guests.

Why IRAs will have more trading flexibility starting May 28th

Posted onMay 26, 2024byRob Hanna

Starting on Tuesday, May 28th the trade settlement process is moving from 2 days to 1 day. This may not sound like a big deal. And if you trade primarily long-term strategies, or only with a margin account, then it isn’t. But for people that would like to incorporate short-term models into their IRA, this is of massive importance.

To demonstrate why, consider a simple model that trades 2 instruments: SPY and SHV. Most brokers will allow you to sell a security and then buy a new security with the cash in an IRA these days. But you can’t flip flop multiple days in a row, because you can not sell a security that you bought with unsettled cash and re-use the unsettled cash before the original trade settles.

Example with current 2-day settlement process:

Day 1: Holding 100% SPY

Day 2: Sell 100% SPY and buy 100% SHV (allowed)

Day 3: Sell 100% SHV and buy 100% SPY (This is not allowed because SPY sale from Day 2 will not settle until Day 4. So you cannot sell SHV and buy back SPY here with a 2-day settlement cycle.)

To make it worse, with all brokers I know, the buys and sells would actually go through, but the account holder would be hit with a violation notice. If this occurs 3 times in a year, then most brokers will halt all trading in the account for an extended period. Others will take away the ability to trade anything on unsettled cash.

If you are trading in a portfolio with lots of securities and frequent ins and outs, tracking what you are allowed to trade and what you aren’t gets even more complicated.

On May 28th with the movement to a 1-day settlement process (T+1), this potential problem goes away. As long as you are not making multiple buys and sells in and out on the same day, these “freeride” violations will not occur.

With my own trading, as well as trading I do for clients at Capital Advisors 360, I utilize several models that are capable of flipping positions after 1 day. The current T+2 settlement has prohibited me from trading some of these models in retirement accounts. But with T+1 arriving, it opens up many new opportunities for IRA holders to take advantage of these short-term models. If you have any questions on this, or if you would like to learn more about Capital Advisors 360 models and whether they could be incorporated into your portfolio, feel free to reach out.

Rob Hanna Wins the 2024 NAAIM Founders Award

Posted onMay 11, 2024byRob Hanna

It was an exciting week here at Quantifiable Edges as it was officially announced that Rob Hanna won the National Association of Active Investment Managers (NAAIM) Founders Award, which is its annual white paper competition.

The paper: Chicken & Egg: Should you use the VIX to time the SPX? Or use the SPX to time the VIX? challenges prevailing market wisdom by suggesting that S&P 500 Index (SPX) action offers a more reliable basis for forecasting the CBOE Volatility Index (VIX) movement than VIX action does in forecasting SPX movement.

If you would like to read the paper, it is available at the NAAIM website, and can also be downloaded from the SSRN website.

If you find the information in the paper appealing and would like to explore VIX-based trading in more detail, you may want to consider checking out the Quantifiable Edges VIX Trading Course.

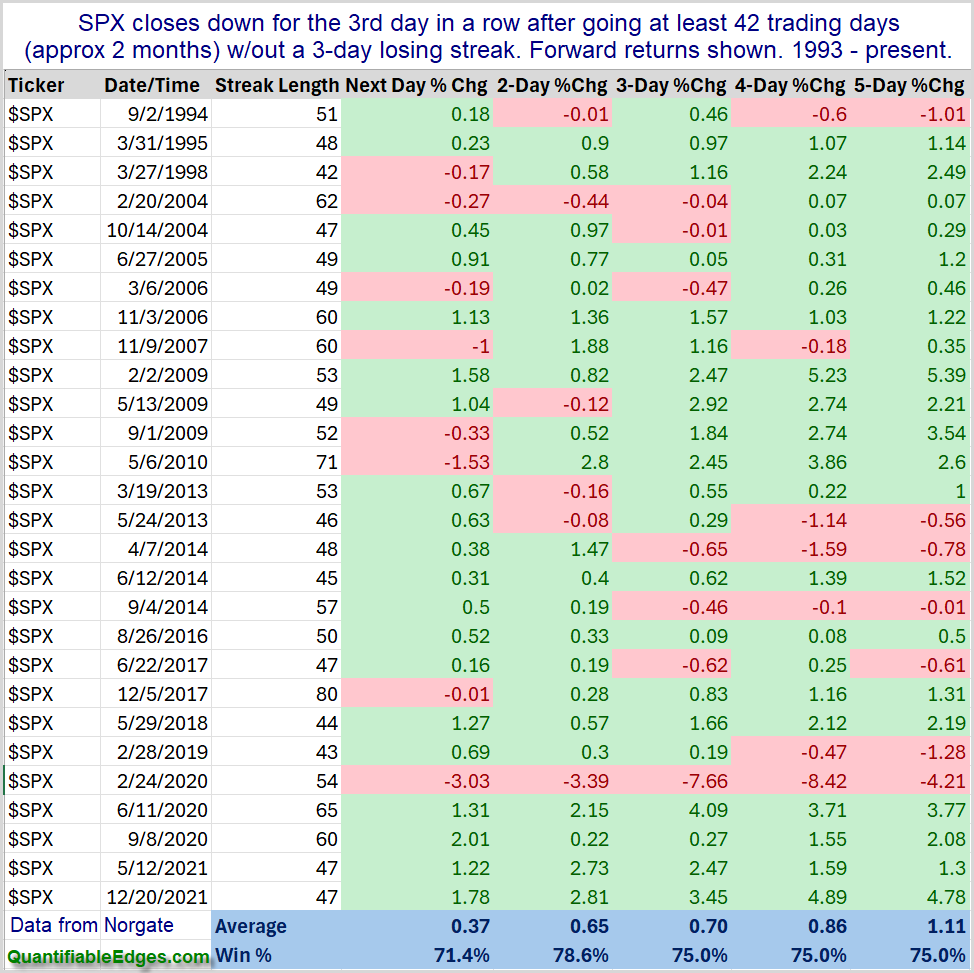

When $SPX has a 3-day pullback for the 1st time in over 2 months…

Posted onMarch 17, 2024byRob Hanna

Friday on X (Twitter) I noted that the 3-day pullback for SPX would be the 1st one since early January. SPX had gone 48 days since the last time it had a 3-day pullback. I looked back at other times SPX went at least 2 months without a 3-day pullback, and examined performance after it finally arrived. This can be seen in the table below.

Results over the next 1-5 days are compelling, and suggest a strong bullish tendency. Traders may want to keep this in mind when setting their short-term market bias.

You must be <a href="https://wislibrary.net/my-account/">logged in</a> to post a review.

$3,170.00Original price was: $3,170.00.$79.00Current price is: $79.00.

We utilize technical analysis concepts and quantify them in a way that allows traders to determine the edge that was provided in the past.

File Size: 7.7 GB.

You must be <a href="https://wislibrary.net/my-account/">logged in</a> to post a review.